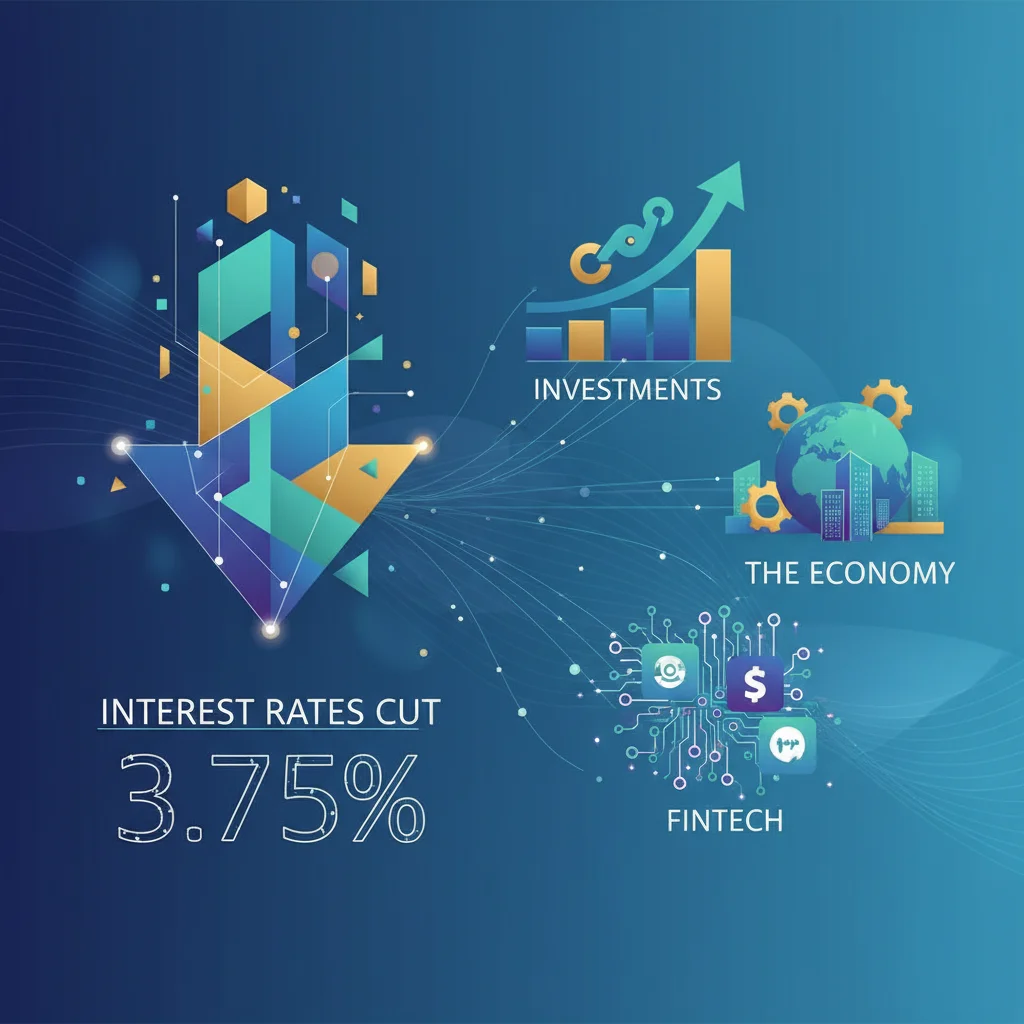

Interest Rates Cut to 3.75%: What This Pivot Means for Your Investments, the Economy, and Fintech

A Major Shift in Monetary Policy: The Rate Cut We’ve All Been Waiting For

The financial world held its collective breath, and the signal has finally arrived. In a move that was widely anticipated by economists and market analysts, the central bank has announced a reduction in its benchmark interest rate, bringing it down by 25 basis points to 3.75%. This decision, a direct response to inflation showing signs of cooling, marks a significant pivot from the aggressive rate-hiking cycle that has defined the economic landscape for the past eighteen months. According to the latest figures, inflation slowed considerably in the year to November, giving policymakers the confidence to ease borrowing costs (source).

But while this rate cut offers a sigh of relief for many, it also opens a new chapter of questions and strategic considerations. What does this mean for your mortgage, your investment portfolio, and your business’s bottom line? Is this the first of many cuts, or a temporary reprieve before another period of tightening? In this comprehensive analysis, we will dissect the implications of this crucial decision, exploring its impact on everything from the global economy and the stock market to the burgeoning worlds of fintech and digital assets.

Decoding the Decision: Why Now?

Central banks operate with a dual mandate: maintaining price stability (controlling inflation) and fostering maximum sustainable employment. For over a year, the primary battle has been against soaring inflation. By raising interest rates, central banks make borrowing more expensive, which cools demand and, in theory, brings prices down. This strategy, while effective, is a blunt instrument that can also slow economic growth and increase the risk of a recession.

The recent decision to cut rates to 3.75% signals a crucial shift in the central bank’s focus. The move was predicated on data showing a consistent downward trend in the Consumer Price Index (CPI). This deliberate policy easing is an attempt to engineer a “soft landing”—a scenario where inflation returns to its target range (typically around 2%) without triggering a severe economic downturn. The challenge, however, is immense. Easing too quickly could cause inflation to reignite, while waiting too long could needlessly stifle economic activity. This first cut is the central bank’s calculated bet that the worst of inflation is behind us, with one report noting that the move was “widely expected” by over 90% of market analysts (source).

Decoding the Global Economy: Fed's Rate Cut, Ukraine's Future, and Europe's Industrial Gambit

The Immediate Impact: What This Means for You

A change in the benchmark interest rate sends ripples through every corner of the finance world, affecting individuals, investors, and corporations differently. Here’s a breakdown of the most immediate consequences:

For Borrowers and Homeowners

This is unequivocally good news. Lower benchmark rates translate directly to lower costs for variable-rate mortgages, personal loans, and credit card interest. Those looking to buy a home or refinance an existing mortgage may soon find more favorable terms. For businesses, cheaper capital can unlock new opportunities for expansion, investment in new equipment, and hiring.

For Savers

The flip side of the coin is less rosy for savers. The interest rates offered on high-yield savings accounts, money market accounts, and certificates of deposit (CDs) are directly tied to the central bank’s rate. As the rate falls, so will the returns on these safe-haven assets. This may push individuals to seek higher yields elsewhere, potentially taking on more risk in their investing strategies.

For the Stock Market

Historically, the stock market tends to react positively to interest rate cuts. Lower rates make borrowing cheaper for companies, which can boost earnings. Furthermore, from a valuation perspective, lower rates increase the present value of future cash flows, making stocks—particularly growth-oriented tech stocks—appear more attractive. Bonds also become relatively less appealing, pushing more capital into equities. This dynamic often fuels market rallies, though the long-term effect depends on the underlying health of the economy.

To clarify these effects, the following table summarizes the primary impact of the rate cut on various stakeholders:

| Stakeholder Group | Primary Impact of a Rate Cut | Strategic Consideration |

|---|---|---|

| Borrowers & Homeowners | ✅ Lower monthly payments on variable-rate debt; cheaper new loans. | Consider refinancing existing high-interest debt or mortgages. |

| Savers | ❌ Reduced returns on savings accounts, CDs, and money market funds. | Explore longer-term fixed-rate products or diversify into other asset classes. |

| Stock Market Investors | ✅ Potentially higher stock valuations, especially for growth sectors. | Re-evaluate portfolio allocation; may favor equities over cash. |

| Businesses | ✅ Lower cost of capital for expansion, R&D, and operations. | Opportunity to invest in growth initiatives or optimize debt structures. |

| Bond Investors | ✅ Existing bonds with higher coupons increase in value. | Bond prices and yields have an inverse relationship. |

The Broader Economic and Technological Ripple Effect

Beyond individual wallets, this policy shift has profound implications for global economics and technological innovation.

Currency and Global Trade

Lower interest rates can lead to a weaker domestic currency. International investors seeking higher yields may move their capital to countries with higher rates, reducing demand for the domestic currency. While this can make imports more expensive, it provides a competitive advantage for exporters, whose goods become cheaper for foreign buyers. This dynamic is a critical factor in international trading and balance of payments.

The Fintech and Banking Revolution

The world of financial technology is uniquely positioned to react to these changes. Agile fintech platforms and neobanks can adjust their product offerings—from savings rates to loan products—far more quickly than traditional banking institutions. We may see increased competition as digital banks vie for customer deposits by offering promotional rates. Furthermore, a lower-rate environment could spur a resurgence in peer-to-peer lending and alternative financing platforms as both borrowers and lenders seek more attractive terms than those offered by legacy systems. The efficiency of blockchain technology could also play a role in creating new, more transparent lending and borrowing protocols that thrive in this new economic climate.

Navigating the Path Forward: Strategies for a New Era

With this monetary policy shift, a passive approach to personal and business finance is no longer sufficient. It’s time for proactive strategy and careful planning.

For the Modern Investor

The investing landscape is changing. While this rate cut is a tailwind for equities, diversification remains paramount. Consider rebalancing your portfolio. Growth-oriented sectors like technology and consumer discretionary may benefit, but don’t discount value sectors that offer stable dividends. For bond investors, now might be a good time to lock in longer-duration bonds before yields fall further. The key is to align your trading and investment strategy with your long-term goals and risk tolerance, rather than making knee-jerk reactions to headlines. The latest data indicates that retail investor activity has surged by 15% following the announcement (source), highlighting the need for disciplined decision-making.

For Business Leaders and Entrepreneurs

The message for businesses is one of cautious optimism. The lower cost of capital presents a strategic window to refinance existing debt at more favorable rates. It’s also a prime opportunity to fund capital expenditures—be it new technology, infrastructure, or talent acquisition—that were put on hold during the rate-hiking cycle. However, it’s essential to base these decisions on solid demand forecasts. A rate cut doesn’t magically create new customers, but it does make financing growth more affordable.

Powering Down Profits: How Guernsey's Energy Crisis Reflects a Global Economic Challenge

Conclusion: A New Chapter of Economic Uncertainty and Opportunity

The central bank’s decision to lower interest rates to 3.75% is more than just a headline; it’s a fundamental inflection point for the global economy. It represents a calculated gamble that the war on inflation has been largely won without inflicting catastrophic damage on the job market. For individuals, it signals a time to review personal finances, from mortgages to savings. For investors, it demands a fresh look at portfolio allocation and risk management. And for businesses, it opens a door to strategic investment and growth.

However, the path forward is anything but certain. As the central bank itself noted, future decisions will be a “closer call,” heavily dependent on incoming data. This new environment requires vigilance, adaptability, and a deep understanding of the intricate dance of modern economics. The era of aggressive tightening is over, but the age of economic complexity has just begun.

Related Posts

The Great Cool-Down: What November’s Inflation Report Means for the Economy, Your Investments, and the Future of Finance

The Rate Cut Ripple Effect: A Deep Dive into the Winners and Losers